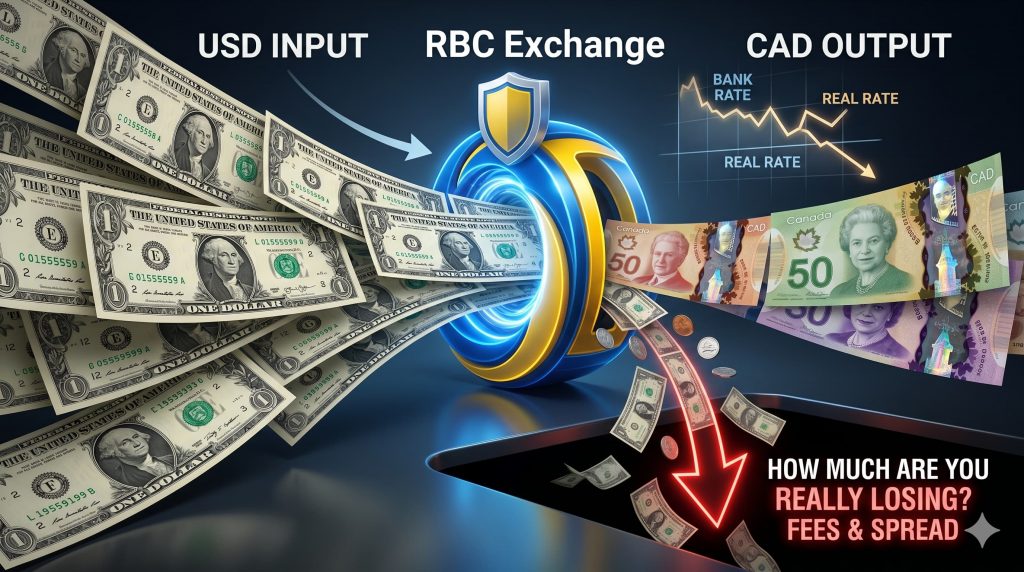

What RBC Charges for USD to CAD Conversions

Royal Bank of Canada is the country’s largest bank by assets, and millions of Canadians use it as their default for everything — including currency exchange. If you’re converting USD to CAD through RBC, whether at a branch, through online banking, or via an international wire, you’re almost certainly paying more than you think.

The issue isn’t that RBC charges a fee you can see on your statement. The cost is baked into the exchange rate itself, and it’s designed to be invisible. Here’s how it actually works and what it costs you in real dollars.

How RBC’s Exchange Rate Markup Works

Every currency exchange starts from the same place: the mid-market rate, also called the interbank rate. This is the wholesale rate that large financial institutions use to trade currencies with each other. You can check it anytime on Google, XE.com, or the Bank of Canada website.

When you convert currency through RBC, you don’t get the mid-market rate. The bank adds a markup — typically 2.5% to 3.5% — and keeps the difference as profit. This markup isn’t disclosed as a separate line item. You simply receive fewer Canadian dollars than the mid-market rate would give you, and the gap is RBC’s revenue.

To put that in perspective: on a mid-market rate of 1.38 CAD per USD, a 3% RBC markup means you’d receive approximately 1.3386 instead of 1.38. On a $10,000 USD conversion, that difference costs you roughly $300 CAD. On $50,000, it’s $1,500.

Real Cost Breakdown by Transaction Size

The following table shows what RBC’s markup costs at different conversion amounts, assuming a mid-market rate of 1.38 and a typical 2.5% to 3% bank spread.

| Amount (USD) | Mid-Market Value (CAD) | Approx. RBC Value (CAD) at 3% markup | Cost of Markup (CAD) |

|---|---|---|---|

| $1,000 | $1,380 | $1,339 | ~$41 |

| $5,000 | $6,900 | $6,693 | ~$207 |

| $10,000 | $13,800 | $13,386 | ~$414 |

| $25,000 | $34,500 | $33,465 | ~$1,035 |

| $50,000 | $69,000 | $66,930 | ~$2,070 |

These numbers are approximate and based on typical RBC retail spreads. The exact markup varies slightly by day and by the channel you use — branch visits, online banking, and wire transfers may each carry a slightly different spread. But the range of 2.5% to 3.5% is consistent with what most RBC customers experience.

Additional Fees on Top of the Markup

The exchange rate spread isn’t the only cost. Depending on how you convert, RBC may charge additional fees that compound the total cost:

- Outgoing wire transfers: RBC charges approximately $45 CAD for outgoing international wires. This is on top of the exchange rate markup, not instead of it.

- Incoming wire transfers: Receiving a wire from a US bank into your RBC account costs $15 to $17 CAD.

- Intermediary bank fees: When wires pass through correspondent banks, each one may deduct a fee from the transfer. You won’t know the amount until the funds arrive, and these fees are outside RBC’s control.

- Non-sufficient funds or returned transfers: If a wire is rejected or returned, additional fees may apply on both ends.

For a detailed breakdown of all the ways banks extract money from currency exchanges, our guide on 7 hidden fees banks charge for currency exchange covers each one in depth.

Why RBC Customers Don’t Notice the Cost

The markup is invisible by design. When you log into RBC online banking and initiate a currency conversion, the system shows you an exchange rate and a final CAD amount. There’s no line item labelled “exchange rate markup — $300.” You see the rate, you accept it, and the money appears in your account.

Most people assume the rate they’re offered is “the” rate — or at least close to it. Without checking the mid-market rate at the same moment, you have no way to calculate the markup. And even if you do check, the comparison requires math that most people aren’t going to do in the middle of a transaction.

This is how banks across Canada generate billions in foreign exchange revenue every year. It’s not that the markup is unfair — banks have overhead, regulatory costs, and risk to manage. It’s that the cost is opaque, and most customers never realize how much they’re paying.

Who’s Most Affected

Any RBC customer who converts currency is paying the markup, but the cost hits some groups harder than others:

- Cross-border workers: If you earn a US salary and convert it to CAD through RBC every payday, you could be losing $200 to $400 per month — or $2,400 to $4,800 per year. Our guide to Canada-US money transfers breaks this down in detail.

- Snowbirds: Converting $30,000 to $50,000 CAD per year for winter living expenses in the US means $750 to $1,750 lost annually to bank markups.

- US property owners: Mortgage payments, property taxes, and maintenance costs in USD add up. Monthly conversions at a 3% markup bleed money over the life of a property.

- Small business owners: Paying US suppliers or receiving USD from American clients? Every invoice converted through RBC costs you 2.5% to 3.5% more than it needs to.

- International students and parents: Tuition payments of $20,000 to $50,000 USD per year at bank rates cost an extra $500 to $1,750 in hidden markup.

How RBC Compares to Other Options

| Provider | Typical Markup (USD/CAD) | Wire Fees | Speed |

|---|---|---|---|

| RBC | 2.5% – 3.5% | $45 outgoing / $15–$17 incoming | 1 – 3 business days |

| Other Big 5 Banks | 2.5% – 3.5% | $30 – $80 depending on bank | 1 – 3 business days |

| Online FX Platforms (e.g., Wise) | 0.4% – 1% | Varies ($0 – $15) | 1 – 2 business days |

| Dedicated FX Providers | 1% – 1.5% | $0 | Same day – next business day |

| Airport Kiosks | 5% – 10% | $0 – $10 commission | Immediate (cash only) |

The takeaway is straightforward: RBC’s rate is better than an airport kiosk but significantly worse than both online platforms and dedicated FX providers. The gap is two to three percentage points — and that’s pure profit margin, not a reflection of any additional service you’re receiving.

How to Check Your Real Cost

Before your next conversion, follow these steps to see exactly what RBC is charging:

- Look up the live mid-market rate on Google, XE.com, or the Bank of Canada website. Note the time.

- Log into RBC online banking and request a quote for the same USD amount.

- Compare the two rates using this formula: Markup % = ((Mid-Market Rate – RBC Rate) ÷ Mid-Market Rate) × 100

- Multiply the markup percentage by your conversion amount to see the dollar cost.

This takes two minutes and will show you exactly how much you’re paying. We’ve found that most RBC customers are genuinely surprised when they see the number for the first time. For a deeper look at how exchange rate margins work across all providers, see our guide to currency exchange margins.

A Better Rate Without Switching Banks

You don’t need to leave RBC to get a better exchange rate. We work alongside your existing bank accounts — there’s no need to close anything or change your day-to-day banking setup.

Here’s how it works: you send us your USD via bank transfer or e-Transfer from your RBC account. We convert it at our rate — typically 1% to 1.5% above mid-market, compared to RBC’s 2.5% to 3.5%. The converted CAD is deposited back into your RBC account (or any Canadian bank account you choose), usually by the next business day.

On a $10,000 USD conversion, switching from RBC’s rate to ours saves you approximately $140 to $270 CAD. On $50,000, the savings jump to $700 to $1,350. Over a year of regular conversions, the difference can reach thousands of dollars.

We’re regulated by FINTRAC, the same federal agency that oversees bank compliance for money services. Client funds are held in a segregated account at a major Canadian financial institution. The process is secure, transparent, and designed to work with the accounts you already have.

Use our currency converter to compare your rate side by side with what RBC offers, or call us at 1-844-915-5151 for a live quote. You can also see how we stack up against all the major banks on our comparison page.